Perhaps you have a vague notion of what open banking is or does, but you’re looking for a clear open banking definition: you’re in the right place. The term open banking refers to enabling third-party software providers and banks to build new, customer-centric financial applications and services with APIs as the enabling technology. But there’s much more to it than that. At its heart, open banking is about giving customers control of their financial data.

Customers allow other third-party organizations to access their data (with their permission) and stimulate innovation in the fintech industry. They exist outside of your banking relationship, although they may be engaged in your online transactions, and there are two types of third-party providers:

- PISP – Payment Initiation Service Provider

- AISP – Account Information Service Provider

You may use a PISP to make online payments without having to enter your credit or debit card information.

An AISP is an internet service provider who has permission to examine specified information from your account. This can include balances and transactions for a set time period.

Now that we understand the role that third-party providers (TPPs) play when it comes to open banking, let’s take a closer look at what open banking is and how it can benefit your business.

What is open banking?

In traditional banking, banks have the highest impact on their existing business models.

However, open banking enables more opportunities to work with fintech companies. It allows you to focus on innovation and create new products that benefit everyone in the ecosystem.

Open banking proponents claim it increases the availability of financial services, like making it easier to exchange financial data with your mortgage lender or accountant. Open banking provides a broad dashboard-style view of your money. It also allows you to do things like link a bank account to a loyalty program. You may also be able to permit a third party to make payments on your behalf from your bank account.

Consumers have come to expect the types of services made possible by open banking; a recent Federal Reserve survey found that nearly seven out of 10 Americans use mobile payment devices to send or receive payments, and more than 60% want a real-time view of their account balance and immediate posting of payments they initiate.

Meanwhile, 83% of those surveyed are using a fintech payment app or digital wallet at least occasionally to complete transactions.

But despite all of the advantages that open banking can offer, it does come with questions of standardization and regulations which banks may find burdensome.

Are there any regulations tied to open banking?

The term Open Banking — with a capital O and B — refers to two different pieces of financial regulation:

- The U.K. Competition and Markets Authority’s (CMA’s) “Open Banking Remedy.”

- European Payment Services Directive 2 (PSD2).

The first one results from an investigation in retail banking by the CMA. This non-governmental British authority has found different holes within the system and has laid out a set of remedies to improve the industry. These include open banking standards.

The second is a European Directive that aims to regulate payment services and payment service providers within the EU. Its main objective is to increase competition and participation in the payments industry and from non-banks. PSD2 launched a first wave of API adoption in European banks, but the European Commission is now discussing a next iteration of the legislation, PSD3, to address PSD2’s shortcomings.

Other countries such as Brazil, Tunisia, Nigeria, or Japan have adopted or are exploring various levels of regulation around open banking as well. Australia took a more holistic view of the issue and introduced the Consumer Data Right (CDR), which applies to banking and finance but extends beyond to other industries.

In North America, Canada has already begun the process of standardizing — notably in order to eliminate screen-scraping — and the U.S. Consumer Financial Protection Bureau announced in late 2022 its intent to propose open banking standardization as well.

Here’s what key industry players agree should happen as open banking comes to North America in 2023.

What are the benefits of open banking?

Open banking APIs are assets for all financial services firms, as they enable them to improve their existing customer engagement, as well as appeal to new prospective customers by meeting their changing demands on accessing their financial information. It also builds new digital revenue channels focusing on banking APIs.

Learn how open banking use cases open up actionable intelligence for banks here.

You may have already used third-party financial management tools that open banking would improve on, apart from the banks, regulators, and startups. Consumers will have more options in managing money, borrowing, and making payments. As Gavin Littlejohn, Chairman of FData Global puts it,

“It’s critically important in the modern world for the customer to be empowered with their financial data to enable them to access products and services which work for them. Not necessarily for the incumbent supplier of their financial services.”

As a consumer, you can connect your bank account with a website or an app that tracks your spending behavior and provide a new product recommendation like a savings account, investment options, or credit cards.

How safe is your data?

Companies involved in open banking should not automatically share consumer data with third parties. Open banking entirely relies on sharing the data, but as a consumer, you retain control and can revoke access to your data at any time.

In Europe, all the products using open banking are required to register with The Competition and Markets Authority’s (CMA’s) “Open Banking Remedy and Financial Conduct Authority (FCA),” either in the UK or via the EU regulators. Since its introduction, Open Banking saw significant growth in the U.K., with seven million people using open-banking enabled products in 2022.

You can also validate the third-party company you use for your financial management tools. They should also tell you on their website or mobile app if they are authorized, along with their registration number.

As long as they are authorized, providers will only have access to the data needed for the service you have signed up for. Make sure to find out how well the third party can secure your information and how they will use your information before sharing your data with them.

Open banking definition “defined”

When you break it down, open banking isn’t hard to define. If you’re using it, you’re allowing a third party to help facilitate your financial transactions.

It’s delivering new benefits to customers and new possibilities for the financial services sector because of governmental action, changing consumer behavior, and the innovation and collaboration spurred by financial technology firms. The concept of open banking isn’t too familiar to the general public, although it is gaining some recognition.

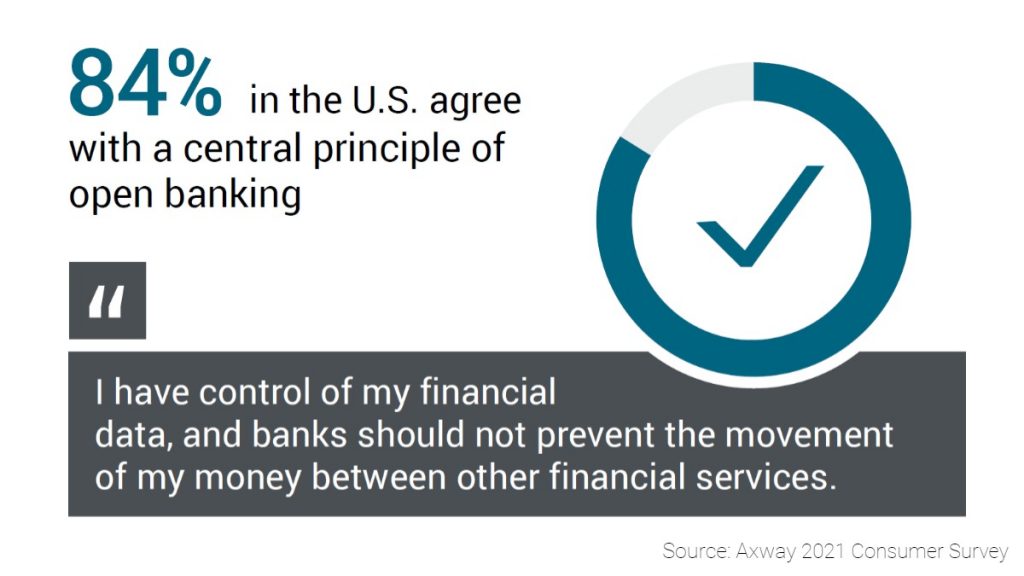

But in one recent survey, 84% of Americans agreed with open banking’s central tenet: that they should have control of their financial data, and banks should not prevent the movement of money between other financial services.

Axway offers financial services solutions

At Axway, we help companies develop innovative goods and services that provide a road to completely integrated finance. We can help improve and customize your consumer interactions with the support of fintechs and other partners.

With Amplify Platform at the center of your strategy, you have the tools and expertise to unleash the full value of your data and unlock all the open banking benefits: offer brilliant customer experiences, create new business services, and accelerate growth in the emerging world of embedded finance.

Coupled with an API marketplace, the solution lets companies govern and control the APIs they need to stay securely connected to customers and partners. Beyond the technology, Axway helps you take your open banking initiative from compliance to business acceleration.

Discover keys to successful adoption of APIs in financial services.

Follow us on social